All Categories

Featured

Table of Contents

Just select any type of level-premium, long-term life insurance policy policy from Bankers Life, and we'll convert your policy without needing proof of insurability. Plans are exchangeable to age 70 or for 5 years, whichever comes later on - aaa direct term life insurance reviews. Bankers Life supplies a conversion debt(term conversion allowance )to insurance policy holders approximately age 60 and with the 61st month that the ReliaTerm policy has actually been in force

They'll offer you with basic, clear options and assist tailor a plan that satisfies your individual needs. You can count on your insurance coverage agent/producer to assist make complex economic choices concerning your future simpler (what is level benefit term life insurance). With a history dating back to 1879, there are some things that never alter. At Bankers Life, that implies taking a personalized strategy to aid secure the people and family members we offer. Our objective is to provide exceptional solution to every insurance holder and make your life much easier when it concerns your insurance claims.

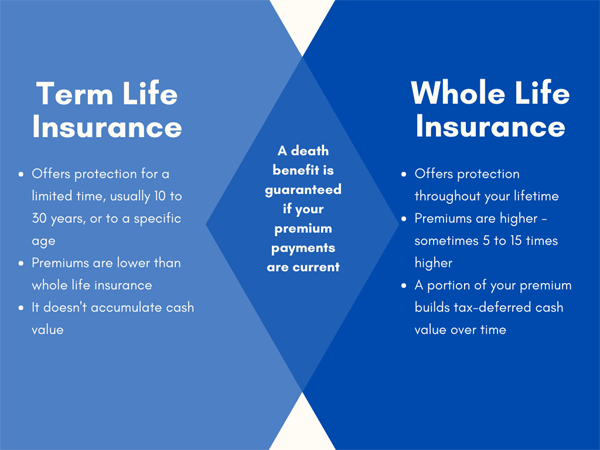

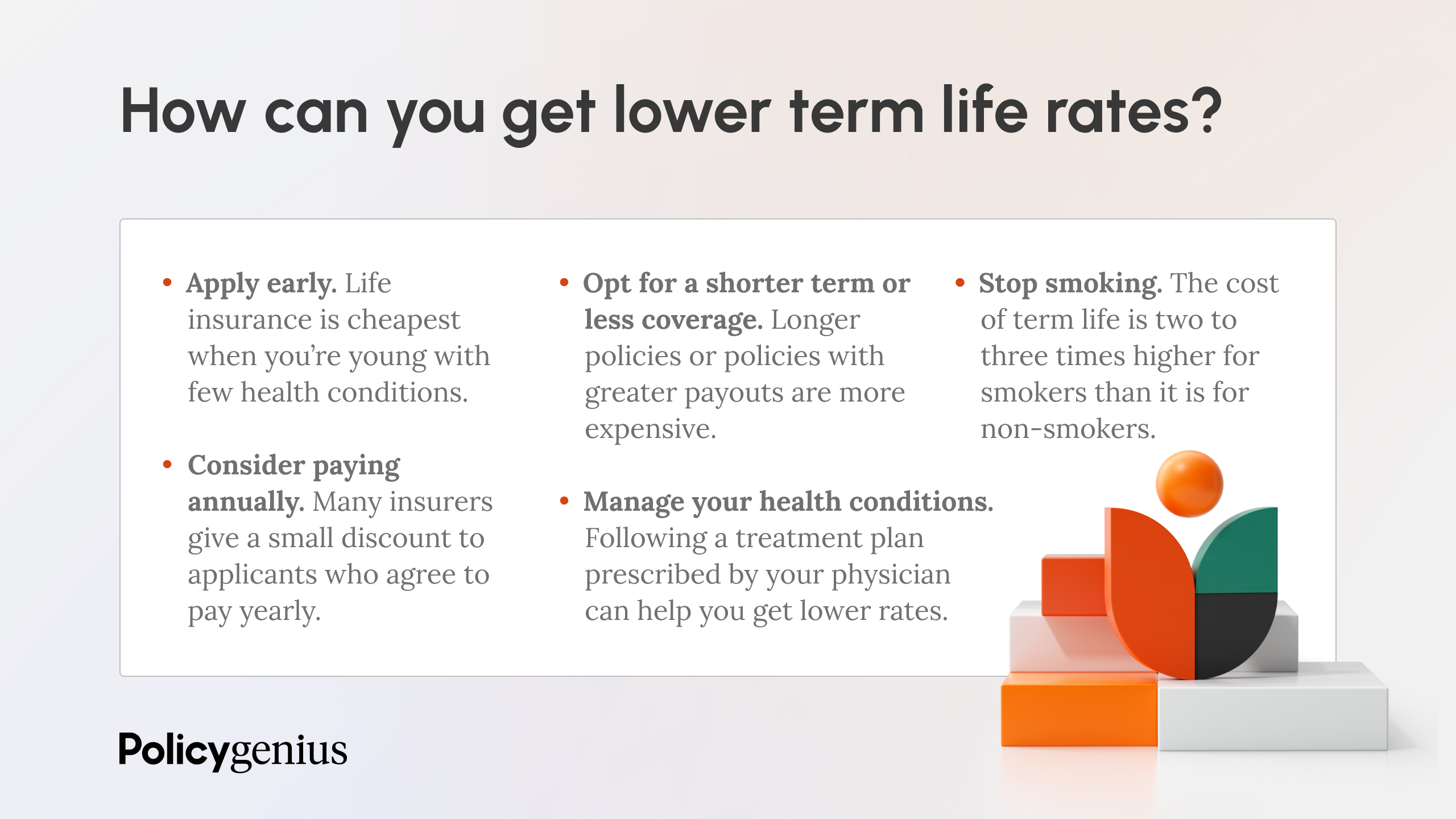

In 2022, Bankers Life paid life insurance policy claims to over 658,000 insurance holders, amounting to$266 million. Bankers Life is accredited by the Better Organization Bureau with an A+ ranking since March 2023, in enhancement to receiving an A( Superb)score by A.M. For the a lot of component, there are 2 sorts of life insurance coverage intends-either term or long-term plans or some mix of both. Life insurers supply different forms of term plans and traditional life policies along with "interest sensitive"items which have ended up being a lot more prevalent given that the 1980's. Term insurance coverage provides defense for a given amount of time. This duration can be as short as one year or provide insurance coverage for a particular number of years such as 5, 10, 20 years or to a defined age such as 80 or in some situations approximately the oldest age in the life insurance policy mortality tables. Presently term insurance coverage prices are really competitive and amongst the most affordable traditionally skilled. It should be kept in mind that it is a widely held belief that term insurance is the least costly pure life insurance coverage offered. One needs to evaluate the plan terms thoroughly to make a decision which term life choices are ideal to satisfy your certain situations. With each brand-new term the costs is increased. The right to renew the policy without evidence of insurability is a crucial benefit to you (spouse term rider life insurance). Or else, the threat you take is that your wellness may degrade and you might be unable to acquire a policy at the exact same prices or perhaps in any way, leaving you and your beneficiaries without coverage. You need to exercise this alternative during the conversion duration. The length of the conversion period will differ depending upon the kind of term policy acquired. If you transform within the proposed period, you are not needed to provide any type of details regarding your wellness. The premium price you

pay on conversion is generally based on your"existing achieved age ", which is your age on the conversion date. Under a level term policy the face quantity of the plan remains the very same for the entire period. With decreasing term the face amount minimizes over the duration. The premium stays the exact same yearly. Commonly such policies are offered as home loan protection with the amount of.

insurance lowering as the balance of the home mortgage decreases. Typically, insurance providers have not can change premiums after the plan is offered. Since such policies might proceed for several years, insurers must utilize conservative death, rate of interest and cost rate price quotes in the premium calculation. Adjustable premium insurance coverage, nevertheless, allows insurance firms to provide insurance policy at reduced" present "costs based upon much less traditional assumptions with the right to transform these costs in the future. Under some policies, premiums are required to be spent for a set number of years. Under various other plans, premiums are paid throughout the policyholder's lifetime. The insurance coverage firm invests the excess costs bucks This kind of plan, which is sometimes called cash money worth life insurance, generates a financial savings element. Money worths are crucial to a long-term life insurance plan. Often, there is no correlation in between the size of the money value and the premiums paid. It is the cash worth of the policy that can be accessed while the insurance policy holder lives. The Commissioners 1980 Criterion Ordinary Mortality Table(CSO )is the current table used in computing minimum nonforfeiture worths and policy gets for average lifeinsurance policies. Many long-term policies will certainly include arrangements, which specify these tax needs. There are two basic classifications of permanent insurance coverage, conventional and interest-sensitive, each with a number of variants. Furthermore, each group is usually readily available in either fixed-dollar or variable form. Typical whole life policies are based upon long-term quotes ofexpense, rate of interest and mortality. If these quotes alter in later years, the business will readjust the costs accordingly but never ever above the maximum ensured costs mentioned in the policy. An economatic whole life plan gives for a basic amount of getting involved entire life insurance policy with an additional extra protection given with using dividends. Because the premiums are paid over a much shorter span of time, the premium payments will certainly be greater than under the whole life strategy. Single costs whole life is minimal payment life where one large superior payment is made. The policy is totally paid up and no additional premiums are needed. Since a significant settlement is involved, it ought to be considered as an investment-oriented item. Rate of interest in single premium life insurance policy is largely because of the tax-deferred treatment of the accumulation of its cash worths. Taxes will certainly be incurred on the gain, nonetheless, when you give up the policy. You may borrow on the cash money worth of the policy, yet remember that you might sustain a substantial tax bill when you surrender, even if you have actually borrowed out all the cash money worth. The advantage is that improvements in rates of interest will certainly be shown more rapidly in interest delicate insurance coverage than in standard; the negative aspect, naturally, is that decreases in rate of interest will certainly also be really felt quicker in passion sensitive entire life. There are four fundamental interest delicate whole life plans: The global life plan is actually greater than rate of interest delicate as it is made to reflect the insurer's existing death and expenditure as well as interest profits as opposed to historical prices. The firm credit scores your premiums to the cash value account. Occasionally the firm subtracts from the cash value account its costs and the cost of insurance security, usually referred to as the mortality reduction fee. The equilibrium of the cash worth account builds up at the rate of interest credited. The company assures a minimal rate of interest and a maximum mortality fee. These warranties are typically very conservative. Present presumptions are crucial to passion sensitive products such as Universal Life. When interest prices are high, advantage estimates(such as money worth)are also high. When rate of interest are low, these projections are not as appealing. Universal life is also one of the most flexible of all the different kinds of policies. The plan usually provides you a choice to pick a couple of sorts of survivor benefit. Under one choice your beneficiaries obtained only the face amount of the plan, under the other they receive both the face amount and the cash money worth account. If you desire the maximum amount of survivor benefit currently, the second choice ought to be chosen. It is vital that these assumptions be realistic because if they are not, you may have to pay more to keep the policy from decreasing or expiring. On the other hand, if your experience is much better then the presumptions, than you might be able in the future to miss a premium, to pay less, or to have the strategy compensated at a very early date. On the various other hand, if you pay more, and your presumptions are sensible, it is feasible to pay up the policy at an early date (term life insurance icon). If you give up a global life policy you might receive much less than the cash money value account due to surrender fees which can be of two types.

You may be asked to make additional premium payments where insurance coverage might terminate because the passion price dropped. The ensured price supplied for in the policy is much lower (e.g., 4%).

Decreasing Term Life Insurance Is No Longer Available

In either case you should obtain a certificate of insurance defining the stipulations of the team policy and any type of insurance coverage cost. Generally the optimum quantity of insurance coverage is $220,000 for a mortgage and $55,000 for all other financial obligations. Credit scores life insurance coverage need not be bought from the company giving the finance

If life insurance policy is called for by a lender as a problem for making a funding, you may have the ability to designate an existing life insurance policy plan, if you have one. However, you might want to buy team credit scores life insurance despite its greater expense due to its ease and its schedule, normally without thorough evidence of insurability.

Nonetheless, home collections are not made and premiums are sent by mail by you to the representative or to the company. There are particular variables that tend to boost the costs of debit insurance greater than regular life insurance policy strategies: Particular expenditures are the exact same whatever the size of the policy, to make sure that smaller sized plans issued as debit insurance will have higher costs per $1,000 of insurance than larger size normal insurance coverage

Considering that early lapses are expensive to a company, the costs should be handed down to all debit insurance policy holders. Since debit insurance coverage is made to consist of home collections, higher commissions and costs are paid on debit insurance coverage than on routine insurance. In a lot of cases these greater expenditures are handed down to the insurance policy holder.

Where a firm has different costs for debit and routine insurance coverage it might be possible for you to purchase a bigger quantity of routine insurance coverage than debit at no added cost - term level life insurance. If you are assuming of debit insurance coverage, you should definitely explore regular life insurance as a cost-saving alternative.

After The Extended Term Life Nonforfeiture Option Is Chosen, The Available Insurance Will Be

This plan is designed for those that can not initially pay for the regular entire life costs yet who want the greater costs coverage and feel they will become able to pay the higher premium (best term life insurance with living benefits). The family policy is a mix strategy that provides insurance protection under one agreement to all participants of your instant household husband, other half and youngsters

Joint Life and Survivor Insurance gives coverage for two or even more persons with the survivor benefit payable at the death of the last of the insureds. Costs are substantially lower under joint life and survivor insurance than for plans that guarantee just one individual, because the probability of having to pay a fatality case is lower.

Costs are significantly more than for policies that insure someone, because the possibility of having to pay a death insurance claim is higher (a whole life policy option where extended term insurance). Endowment insurance coverage attends to the settlement of the face quantity to your beneficiary if fatality happens within a details amount of time such as twenty years, or, if at the end of the particular duration you are still to life, for the payment of the face total up to you

{kind=link}

Latest Posts

A Whole Life Policy Option Where Extended Term Insurance Is Selected Is Called A(n)

Affordable Funeral Insurance

Final Expense Life Insurance Policy